Chapter 5: Saving and Borrowing for a Household

David and Linda Evans live in Tralee, Co. Kerry with their three children. David is a teacher and Linda is a paramedic. They want to save for their children's future education.

Reason: Savings earn interest, which means the amount saved increases in value each year.

Financial Institution 2: Credit Union

Reason: Regular saving with a credit union builds a positive record with them, which makes it easier to get a loan from them in the future.

Other acceptable institutions: An Post, Building Society. Other acceptable reasons: Deposits are protected by the Deposit Guarantee Scheme (Commercial Bank). Some accounts are exempt from DIRT (An Post).

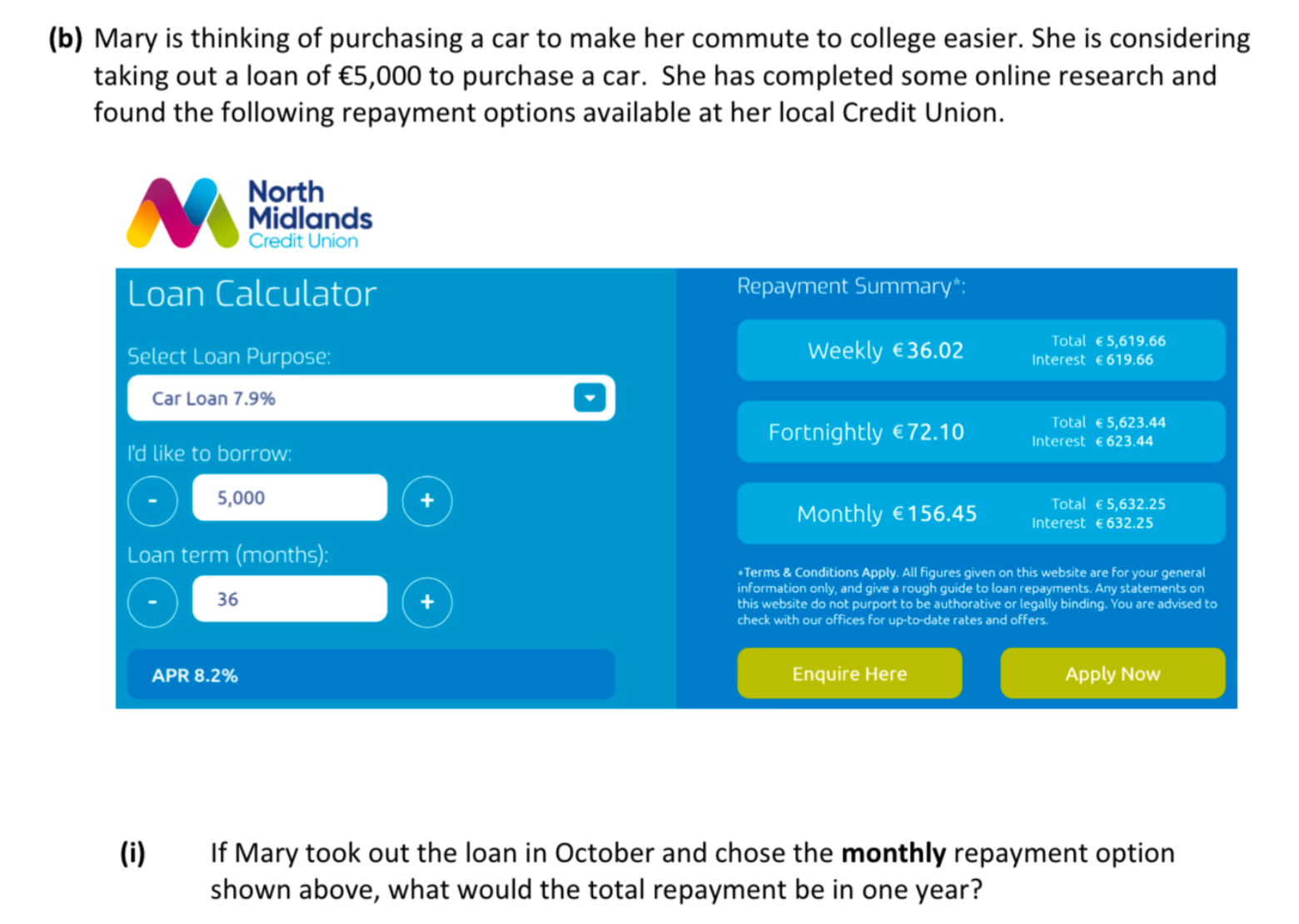

Mary is thinking of purchasing a car to make her commute to college easier. She is considering taking out a loan of €5,000. The credit union shows monthly repayments of €156.45 over 36 months.

Interest paid: €5,632.20 - €5,000 = €632.20

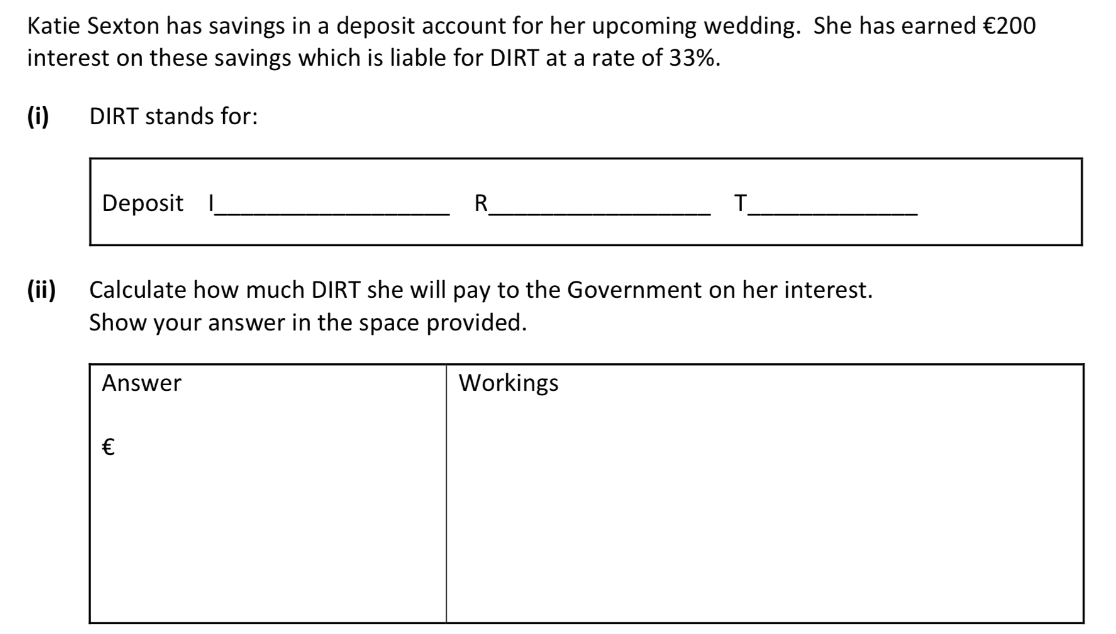

Katie Sexton has savings in a deposit account for her upcoming wedding. She has earned €200 interest on these savings, which is liable for DIRT at a rate of 33%.

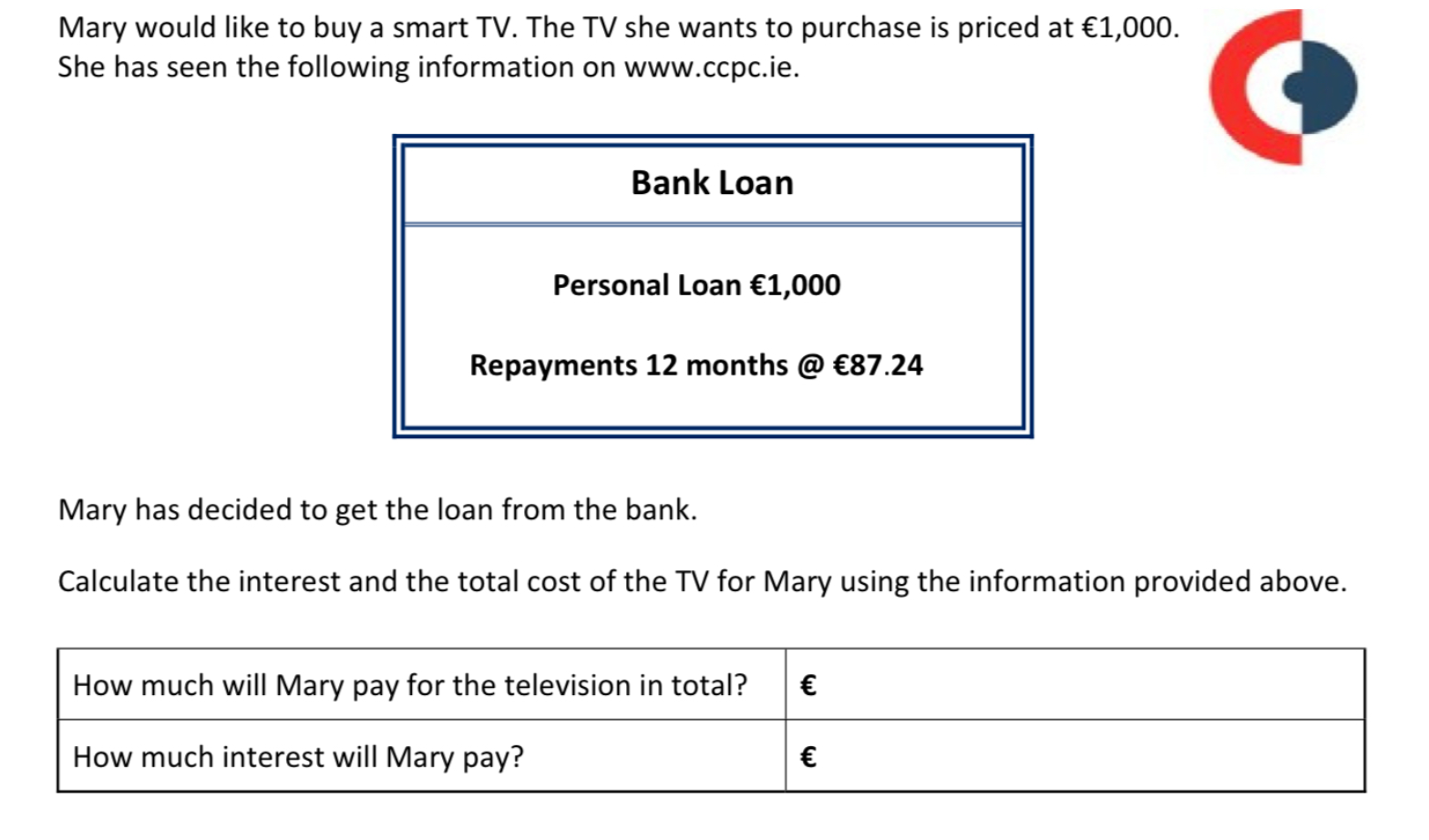

Mary would like to buy a smart TV priced at €1,000. She has seen a bank loan offer on www.ccpc.ie: Personal Loan €1,000, repayments 12 months at €87.24 per month.

Interest paid: €1,046.88 - €1,000 = €46.88

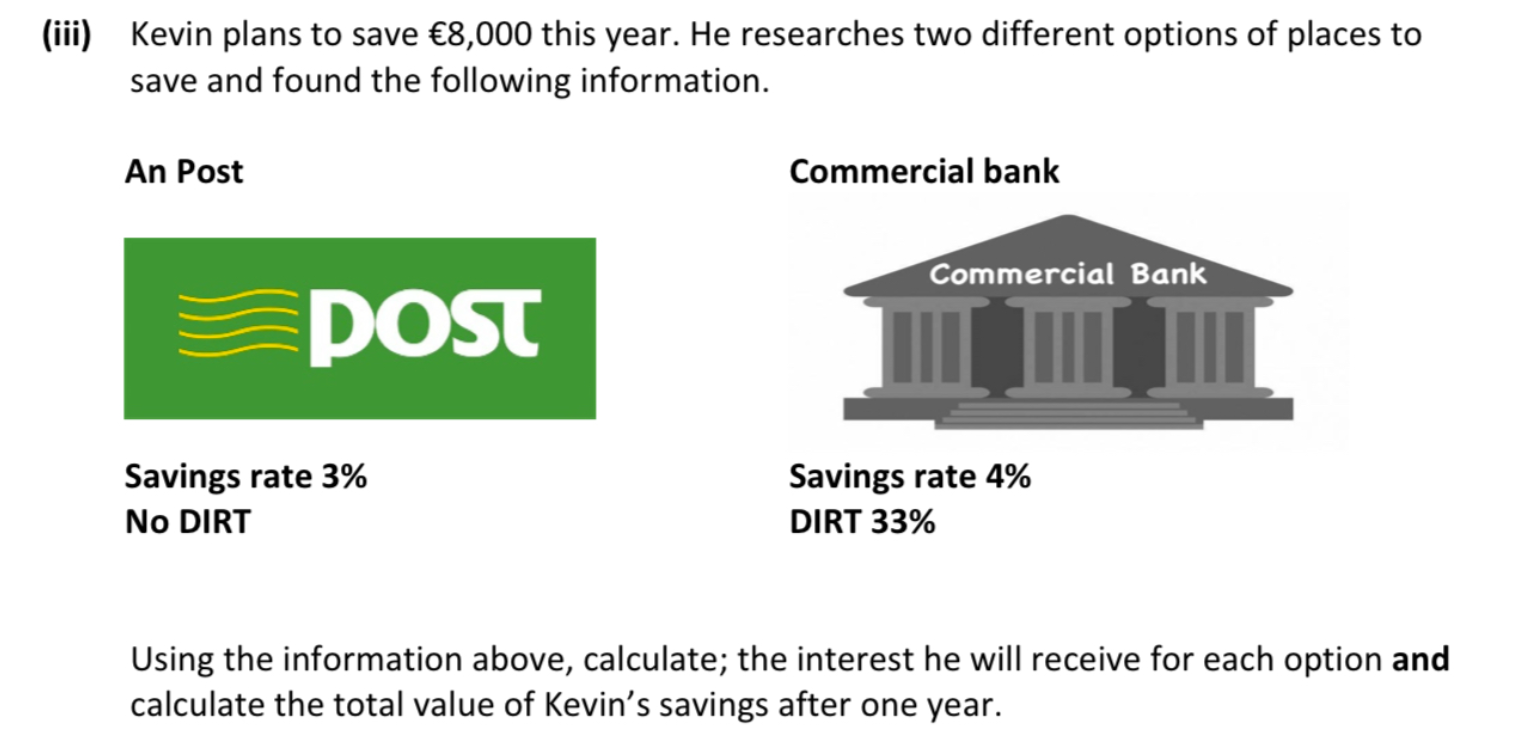

Kevin has a steady income and has decided to start saving. He plans to save €8,000 and has researched two options: An Post (savings rate 3%, no DIRT) and a Commercial Bank (savings rate 4%, DIRT 33%).

1. For future planned expenditure (such as a family event or buying a car)

2. For emergencies or unplanned events (such as in case a car breaks down)

3. To earn interest on savings

4. To provide income in retirement

5. To improve a credit rating

Interest: €8,000 x 3% = €240

Total savings: €8,000 + €240 = €8,240

Commercial Bank:

Interest: €8,000 x 4% = €320

DIRT: €320 x 33% = €105.60

Interest after DIRT: €320 - €105.60 = €214.40

Total savings: €8,000 + €214.40 = €8,214.40

When interest rates are high, it encourages saving. When interest rates are low, it encourages borrowing.

Borrowing: Interest is the financial cost charged by a financial institution for borrowing money.

Interest is usually expressed as a percentage, such as an Annual Percentage Rate (APR).

| Purchase | Source of Finance |

|---|---|

| House | (your answer) |

| Car | (your answer) |

| Groceries | (your answer) |

Car: Hire Purchase / Medium-term loan

Groceries: Credit card / Bank overdraft