JC

HUB

HUB

Personal Insurance

Ch6

LO 1.6

LO 1.6

📌 Tap each section to expand it.

🛡 Chapter 6 — Personal Insurance

What Is Insurance?

▼

Insurance helps people manage risk. It protects against the financial cost of unexpected events.

People pay a premium to an insurance company. The company pools these payments and pays compensation if something goes wrong.

Why get insurance? (1) Financial protection against large costs. (2) Legal requirement (motor). (3) Reduces financial stress and worry.

Types of Insurance

▼

Motor: cover for accidents, theft and damage. Third party or comprehensive.

House: cover for damage to the building and contents from fire, theft or flooding.

Health: cover for private medical treatment and operations.

Travel, Gadget, Pet: cover for holiday emergencies, device repair/replacement, veterinary costs.

Life Assurance: pays a lump sum to the family if the person dies. Not the same as other types of insurance.

Top Tip: Do not use Life Assurance as a type of insurance in exam answers. It covers an event that will definitely happen, not an event that may or may not happen.

Cost of Insurance (Premiums)

▼

Premium = the payment made to an insurance company to keep a policy active. Higher risk = higher premium.

Factors: age/experience, value of item, location, level of cover, claims history, security features.

Loading = extra charge added because the risk is higher. Loadings increase the premium.

Reduction = discount applied to bring the premium down. Examples: no claims bonus, alarm fitted, paying annually.

Top Tip: Use any information given in the question. If it says “21 years of age” or “old car”, write that in your answer and explain why it affects the premium.

Policy Excess & Reducing Premiums

▼

Policy excess = the amount the insured person pays first before the insurance company covers the rest. Claim payout = damage - excess.

Higher excess = lower premium (you agree to cover more of the cost yourself).

Ways to reduce premium: install security, build up NCB, pay annually, increase excess, buy online, shop around (Bonkers.ie / insurance broker).

Principles of Insurance

▼

Utmost Good Faith: all material facts must be disclosed when applying.

Insurable Interest: must have a financial interest in the item being insured.

Indemnity: a profit cannot be made from insurance. Restored to same position as before the loss.

Contribution: if insured with more than one company, they share the cost of the claim.

Subrogation: after paying a claim, the insurer can pursue the person responsible to recover costs.

📚 Tap any term to reveal its definition.

Insurance Basics

Risk

The chance that something unexpected could happen that costs a person money.

+

Insurance

A way of protecting against the financial cost of unexpected events. People pay a premium to an insurance company which agrees to cover the cost if something goes wrong.

+

Premium

The payment made to an insurance company, usually monthly or annually, to keep a policy active. Higher risk = higher premium.

+

Claim

A request made by the insured person to the insurance company for compensation after a loss or accident.

+

Compensation

The money paid out by the insurance company to the insured person after a valid claim.

+

Premiums & Calculations

Loading

An extra charge added to a premium because the insurer considers the risk to be higher than normal. A percentage increase on the base premium.

+

Reduction

A discount applied to a premium that lowers the cost. Given because the risk is lower or as an incentive to attract customers.

+

No Claims Bonus (NCB)

A percentage discount earned for each year a driver goes without making a claim. Up to 60% discount after five claim-free years.

+

Policy Excess

The amount the insured person must pay first before receiving the rest of the claim from the insurance company. Higher excess = lower premium.

+

Principles of Insurance

Utmost Good Faith

All material facts must be disclosed when applying for insurance. The insured person must tell the truth about anything that could affect the cost or the decision to provide cover.

+

Insurable Interest

The insured must have a financial interest in the item being insured. They must suffer financially if there is damage or loss.

+

Indemnity

A profit cannot be made from insurance. The insured should be restored to the same financial position as before the loss.

+

Contribution

When the same risk is insured with more than one company, the insurers share the cost of any claim between them.

+

Subrogation

After paying out on a claim, the insurance company can take legal action against the party responsible for the loss to recover its costs.

+

🎦 Chapter 6 video walkthroughs. VIDEOS TO BE ADDED THIS WEEK

What Is Insurance and Why Do We Need It?

Risk, premiums, types of insurance and why motor insurance is a legal requirement.

Calculating Premiums: Loadings, Reductions and Policy Excess

How to calculate premiums with loadings and reductions, and how policy excess works.

Principles of Insurance

Utmost Good Faith, Insurable Interest, Indemnity, Contribution and Subrogation explained with examples.

⚡ Work through the pile. Tap to flip. Tick when you know it.

🅻 Test yourself. Pick a topic or try all.

📄 Past paper questions with model answers.

Key Skills Tested (2019-2025)

① Explain key insurance terms (premium, loading, excess, NCB)

② Identify types of insurance for different needs

③ Identify factors affecting the cost of a premium

④ Calculate premiums using loadings and reductions

⑤ Calculate compensation after applying a policy excess

⑥ Match principles of insurance to definitions

⑦ Read a chart to identify trends in premiums

② Identify types of insurance for different needs

③ Identify factors affecting the cost of a premium

④ Calculate premiums using loadings and reductions

⑤ Calculate compensation after applying a policy excess

⑥ Match principles of insurance to definitions

⑦ Read a chart to identify trends in premiums

📄 2025 Paper — Q11 6m

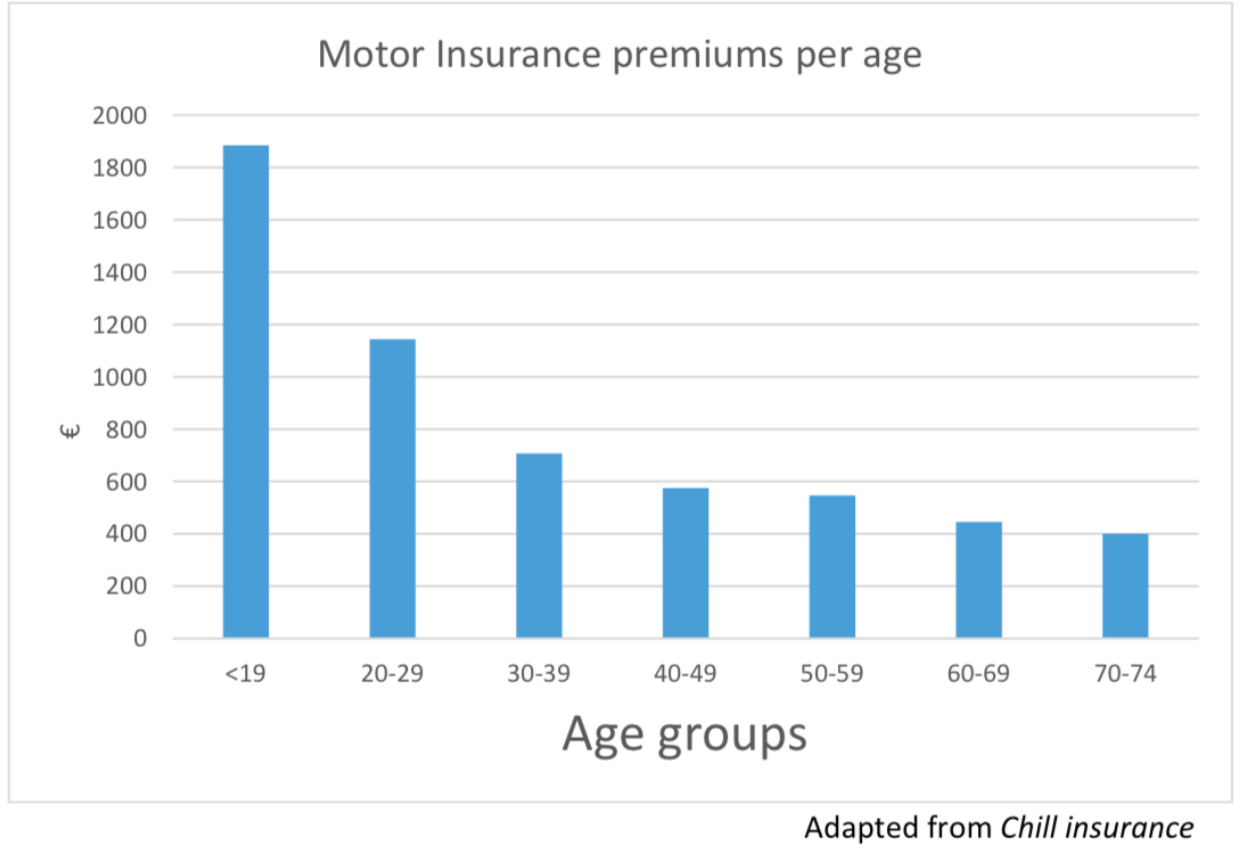

(i) Explain the term insurance premium. (ii) What does the chart show about motor insurance premiums?

Top Tip: Use figures from the chart. Stating a trend alone without figures may not get full marks.

(i) The premium is the payment/fee for insurance cover. It is how much it costs to insure your property for a period of time. It is paid by the insured person. Higher risk = higher premium.

(ii) Average motor insurance premiums decrease as a driver gets older. Not everybody pays the same, for example 20-29 year olds pay approximately €1,100 whereas 60-69 year olds pay approximately €500.

(ii) Average motor insurance premiums decrease as a driver gets older. Not everybody pays the same, for example 20-29 year olds pay approximately €1,100 whereas 60-69 year olds pay approximately €500.

📄 2024 Paper — Q3 6m

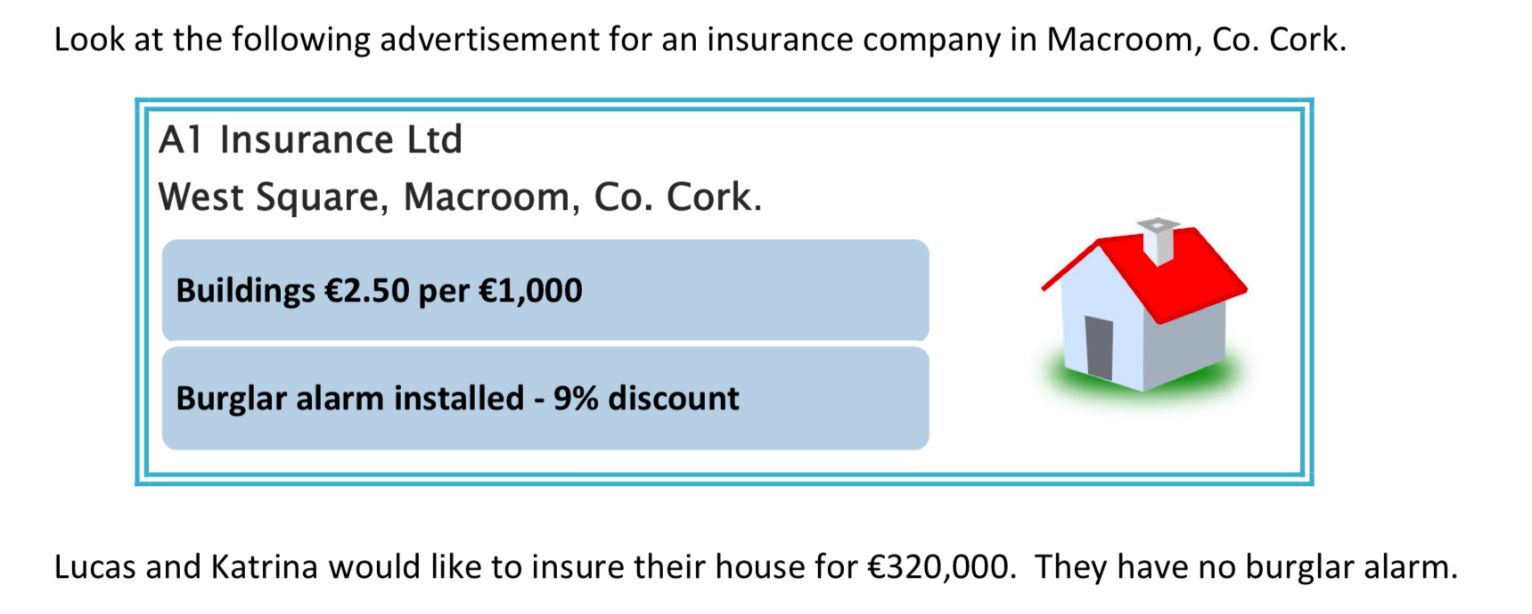

Lucas and Katrina insure their house for €320,000. No burglar alarm. (i) Calculate the premium. (ii) Calculate the saving if they install a burglar alarm.

Top Tip: Read the question carefully. Part (ii) asks for the saving, not the new premium. Some students wrote €728 (the new premium) instead of €72 (the saving).

(i) €320,000 ÷ €1,000 = 320. 320 × €2.50 = €800.

(ii) €800 × 9% = €72 saving.

(ii) €800 × 9% = €72 saving.

📄 2023 Paper — Q10 6m

Identify three types of insurance a family might purchase.

Top Tip: Do not use Life Assurance here. Life Assurance covers an event that will happen (death). Other insurance covers events that may or may not happen. Motor is the type of insurance, not comprehensive or 3rd party — make sure to say motor or car insurance and not a type of motor or car insurance.

Any three: Motor/Car, House/Home/Buildings, Health, Travel, Pet, Dental, Gadget.

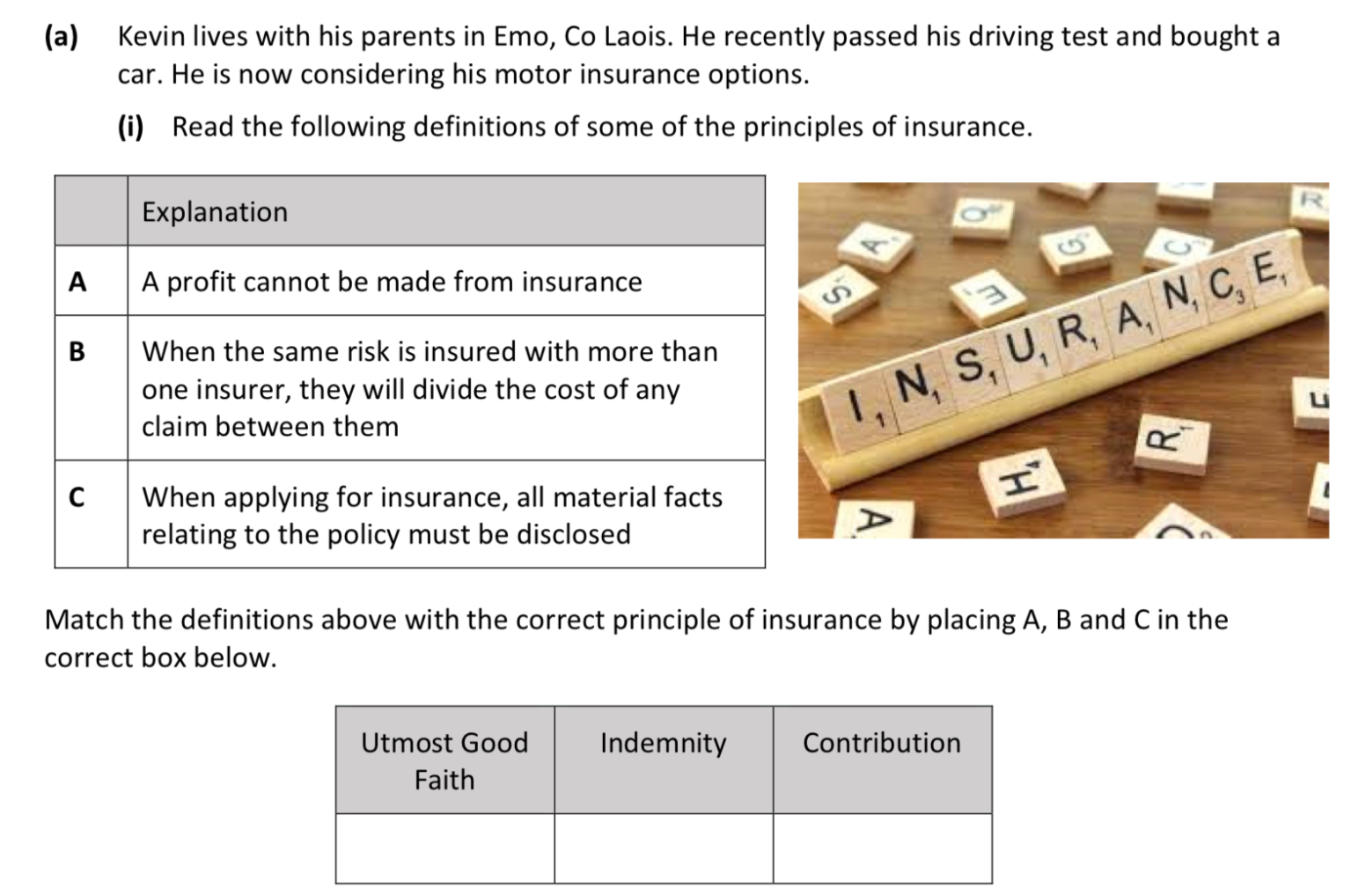

📄 2022 Paper — Q18(a)(i) 9m

Match definitions A, B, C to the correct principle: Utmost Good Faith, Indemnity, Contribution.

| Utmost Good Faith | Indemnity | Contribution |

|---|---|---|

| C - all material facts must be disclosed | A - a profit cannot be made from insurance | B - insurers divide the cost of any claim between them |

📄 2022 Paper — Q18(a)(v)(vi) 6m

Kevin has comprehensive insurance, policy excess €500. Accident causes €2,500 damage. (v) Calculate compensation. (vi) Impact on next year's premium.

Top Tip: Two impacts here: higher premium next year AND loss of no claims bonus. Both are worth mentioning.

(v) €2,500 - €500 = €2,000 compensation.

(vi) Kevin will have to pay a higher premium next year as a result of making a claim. He will also lose his no claims bonus/discount.

(vi) Kevin will have to pay a higher premium next year as a result of making a claim. He will also lose his no claims bonus/discount.

📄 2019 Paper — Q4 6m

Gerard is 21 and just passed his driving test. He bought an old car. Outline two factors the insurance company will consider when calculating the cost.

Top Tip: Use the information given. The question says “21 years of age” and “old car”, so include these details and explain why they affect the premium.

1. Gerard is young (21) with little driving experience, increasing the risk of an accident, so the premium will be higher.

2. Gerard has an old car, which is generally lower in value, reducing the cost of compensation if damaged, so the premium may be lower.

Other acceptable factors: previous claims, penalty points, type of cover, location, make and model of car.

2. Gerard has an old car, which is generally lower in value, reducing the cost of compensation if damaged, so the premium may be lower.

Other acceptable factors: previous claims, penalty points, type of cover, location, make and model of car.