Household Budgets

Ch12

LO 1.12

LO 1.12

📌 Tap each section to expand it.

📈 Chapter 12 — Household Budgets

What Is a Household Budget & Why Prepare One?

▼

Household Budget — a plan showing a household’s expected future income and expected future expenditure over a period of timeHelps a household work out its future financial position

Live within their means — plan to avoid spending more than is earned, reducing the risk of falling into debt

Reduce impulse buying — a spending plan makes unplanned purchases less likely

Identify when borrowing may be required — highlights months when expenditure is higher than income, so finance can be arranged in advance

Identify where to cut back — breaks expenditure into fixed, irregular and discretionary categories to spot areas where spending could be reduced

Help save for the future — helps a household set aside enough income each month to prepare for future costs such as a car or holiday

Calculating Planned Income

▼

Planned Income — every source of income the household expects to receive, listed separately for each monthSources include: wages, salary, Child Benefit, Jobseeker’s Benefit, pension, commission, overtime

Regular income — stays the same each month, such as a salary or Child Benefit

Irregular income — only appears in certain months, such as overtime or a bonusTotal income can vary month to month because of this

Total Income (A) — all sources of planned income added together for each month

Top Tip: Income that changes in a specific month should be adjusted in that column only. All other months stay the same.

Calculating Planned Expenditure

▼

Fixed Expenditure — a set payment made at a set time each month; the amount does not changeExamples: mortgage, rent, car loan repayment, TV licence, house insurance

Irregular Expenditure — spending that varies in amount and timing each monthExamples: groceries, electricity, car running costs, phone bills, clothing

Discretionary Expenditure — non-essential spending a household can choose to spend on or notExamples: holidays, entertainment, gifts, restaurant meals, TV subscriptions

Total Expenditure (B) — fixed subtotal + irregular subtotal + discretionary subtotal added together for each month

Net Cash, Opening Cash & Closing Cash

▼

Net Cash = Total Income (A) minus Total Expenditure (B)Positive = surplus that month • Negative = deficit that month (shown in brackets)

Opening Cash — the cash available at the start of each monthOpening cash in the Total column is always the same as the opening cash for the first month — it is given in the question

Closing Cash = Net Cash + Opening CashClosing cash for one month becomes the opening cash for the next month

Top Tip: Negative figures must always be shown in brackets, for example (€340). Do not use a minus sign.

Financial Position, Surplus & Deficit

▼

Strong financial position — closing cash is positive every month and growing over the budget periodOptions: build an emergency fund, save for a large future purchase

Weak financial position — closing cash is negative or turns negativeThe household is living beyond its means

Budget Surplus — total planned income is greater than total planned expenditure across the budget periodOptions: save or invest, plan a large future spend, repay a loan early

Budget Deficit — total planned expenditure is greater than total planned incomeActions: reduce discretionary spending, increase income, shop around for better value, spread payments over time

Revising a Budget & Analysing Graphs

▼

Revising a Budget — when income or expenditure changes, the budget must be updatedCommon reasons: pay rise, pay cut, reduced hours, new expense such as a loan repayment

Impact of a revision — always state direction of change and use figuresExample: “Net cash will decrease from a surplus of €500 to a deficit of (€200)”

Top Tip: When a question says “based on their budget” or “based on the graph”, always include a specific € figure from it. A general answer without a number may not get full marks.

📚 Tap any term to reveal its definition.

What Is a Household Budget

Household Budget

A plan that shows a household’s expected future income and expected future expenditure over a period of time. It helps a household work out its future financial position.

+

Planned Income

Every source of income the household expects to receive, listed separately for each month. Sources include wages, salary, Child Benefit, Jobseeker’s Benefit, pension, commission and overtime.

+

Planned Expenditure

All spending a household expects to make over the budget period, divided into three categories: fixed, irregular and discretionary.

+

Types of Expenditure

Fixed Expenditure

A set payment made at a set time each month. The amount does not change. Examples: mortgage or rent, car loan repayment, TV licence, house insurance.

+

Irregular Expenditure

Spending that varies in amount and timing each month depending on usage. Examples: groceries, electricity bills, car running costs, phone bills, clothing.

+

Discretionary Expenditure

Non-essential spending that a household can choose to spend on or not. Examples: holidays, entertainment, gifts, restaurant meals, TV subscriptions.

+

Budget Calculations

Total Income (A)

All sources of planned income added together for each month.

+

Total Expenditure (B)

The fixed subtotal, irregular subtotal and discretionary subtotal added together for each month.

+

Net Cash

Total Income (A) minus Total Expenditure (B). A positive figure means a surplus that month. A negative figure means a deficit that month. Negative figures are always shown in brackets.

+

Opening Cash

The cash available at the start of each month. Opening cash in the Total column is always the same as the opening cash for the first month. It is given in the question.

+

Closing Cash

The cash a household expects to have at the end of each month. Closing Cash = Net Cash + Opening Cash. The closing cash for one month becomes the opening cash for the next month.

+

Financial Position

Budget Surplus

When total planned income is greater than total planned expenditure across the full budget period. Options: save or invest, plan a large future spend, repay a loan early.

+

Budget Deficit

When total planned expenditure is greater than total planned income. Actions: reduce discretionary spending, increase income, shop around for better value, spread large payments over time.

+

Living Beyond Their Means

When a household plans to spend more than it has available. This is shown by a negative closing cash figure. The household will need to reduce spending or increase income to address this.

+

Strong Financial Position

When closing cash is positive every month and growing over the budget period. The household can build an emergency fund or save for a large future purchase.

+

Weak Financial Position

When closing cash is or turns negative. The household is living beyond its means and needs to take action such as reducing discretionary spending or increasing income.

+

Video coming soon.

The Chapter 12 video will appear here once it has been uploaded.

The Chapter 12 video will appear here once it has been uploaded.

Tap the card to flip it

Still learning 15

📄 Past paper questions for Chapter 12. Show the model answer only after you have tried the question yourself.

2025 — Q16 (b)(i) — Outline two reasons why households prepare a budget

6 marksA budget is an essential part of running any family household.

Outline two reasons why family households should prepare a budget.

Outline two reasons why family households should prepare a budget.

Reason 1: To plan their future expenditure so they ensure that they live within their means and avoid falling into debt.

Reason 2: To calculate their closing cash balance at the end of each future month so that they can adjust spending or arrange borrowing if it will be a negative figure.

Reason 2: To calculate their closing cash balance at the end of each future month so that they can adjust spending or arrange borrowing if it will be a negative figure.

Top Tip: For any “outline a reason” question, always give two parts — the action and the outcome. Do not just write “to plan spending”. Write “to plan their future spending so they can ensure they live within their means”.

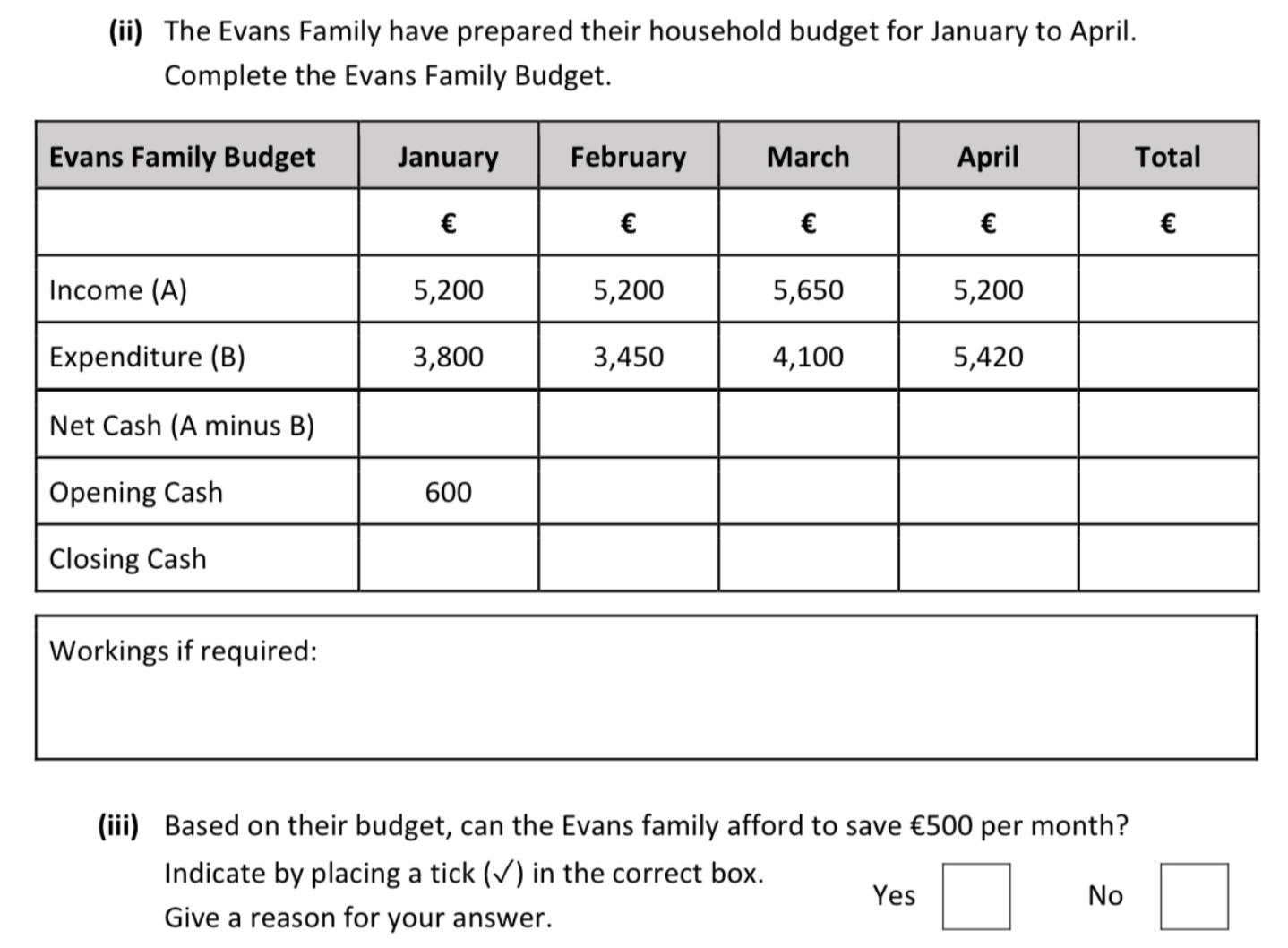

2025 — Q16 (b)(ii) — Complete the Evans Family Budget

16 marks

The Evans Family have prepared their household budget for January to April. Fill in the blank boxes to complete the Evans Family Budget.

Opening cash January: €600

Opening cash January: €600

| Evans Family Budget | Jan € | Feb € | Mar € | Apr € | Total € |

|---|---|---|---|---|---|

| Income (A) | 5,200 | 5,200 | 5,650 | 5,200 | 21,250 |

| Expenditure (B) | 3,800 | 3,450 | 4,100 | 5,420 | 16,770 |

| Net Cash | 1,400 | 1,750 | 1,550 | (220) | 4,480 |

| Opening Cash | 600 | 2,000 | 3,750 | 5,300 | 600 |

| Closing Cash | 2,000 | 3,750 | 5,300 | 5,080 | 5,080 |

Top Tip: Closing cash for one month becomes the opening cash for the next. The April closing cash of €5,080 is also the Total closing cash. The opening cash in the Total column is always the same as January opening cash: €600.

2025 — Q16 (b)(iii) — Can the Evans family afford to save €500 per month?

3 marksBased on their budget, can the Evans family afford to save €500 per month? Yes or No? Give a reason for your answer using figures from the budget.

Yes. Saving €500 per month over 4 months totals €2,000. The Evans family has a total net cash of €4,480 over the period, meaning they plan to have significantly more income coming in than going out even after saving (€4,480 − €2,000 = €2,480 remaining).

Top Tip: When a question says “based on their budget”, always include a specific € figure. A general answer without a number may not get full marks.

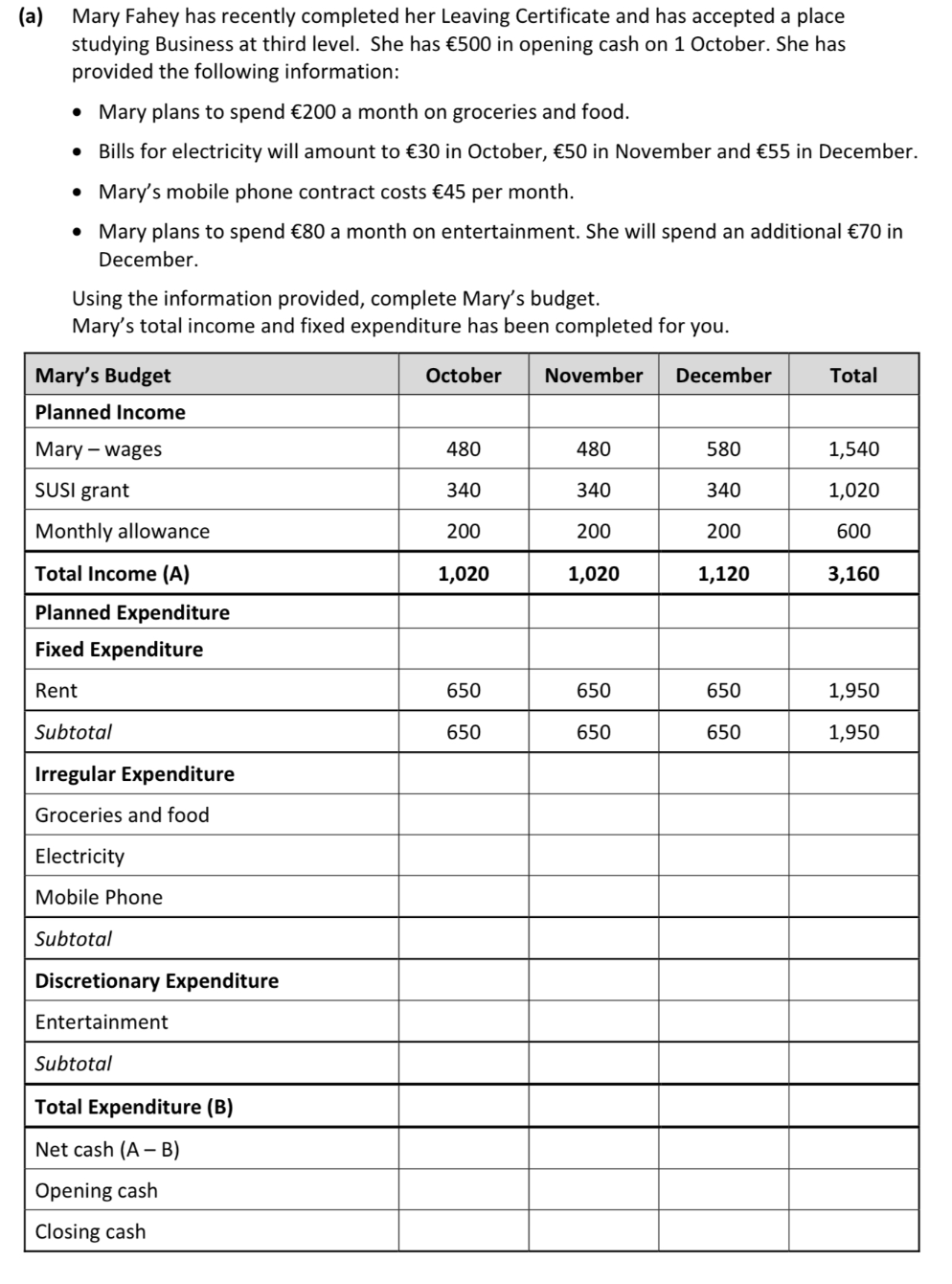

2024 — Q18 (a) — Complete Mary Fahey’s Budget

32 marks

Mary Fahey has recently completed her Leaving Certificate. She has €500 in opening cash on 1 October. Complete Mary’s budget using the information provided. Total income and fixed expenditure have been completed for you.

Irregular expenditure: Groceries: €200 each month (€600 total). Electricity: Oct €30, Nov €50, Dec €55 (€135 total). Mobile phone: €45 each month (€135 total). Subtotals: Oct €275, Nov €295, Dec €300, Total €870.

Discretionary: Entertainment: Oct €80, Nov €80, Dec €150 (€310 total).

Total Expenditure (B): Oct €1,005 / Nov €1,025 / Dec €1,100 / Total €3,130

Net Cash: Oct €15 / Nov (€5) / Dec €20 / Total €30

Opening Cash: Oct €500 / Nov €515 / Dec €510 / Total €500

Closing Cash: Oct €515 / Nov €510 / Dec €530 / Total €530

Discretionary: Entertainment: Oct €80, Nov €80, Dec €150 (€310 total).

Total Expenditure (B): Oct €1,005 / Nov €1,025 / Dec €1,100 / Total €3,130

Net Cash: Oct €15 / Nov (€5) / Dec €20 / Total €30

Opening Cash: Oct €500 / Nov €515 / Dec €510 / Total €500

Closing Cash: Oct €515 / Nov €510 / Dec €530 / Total €530

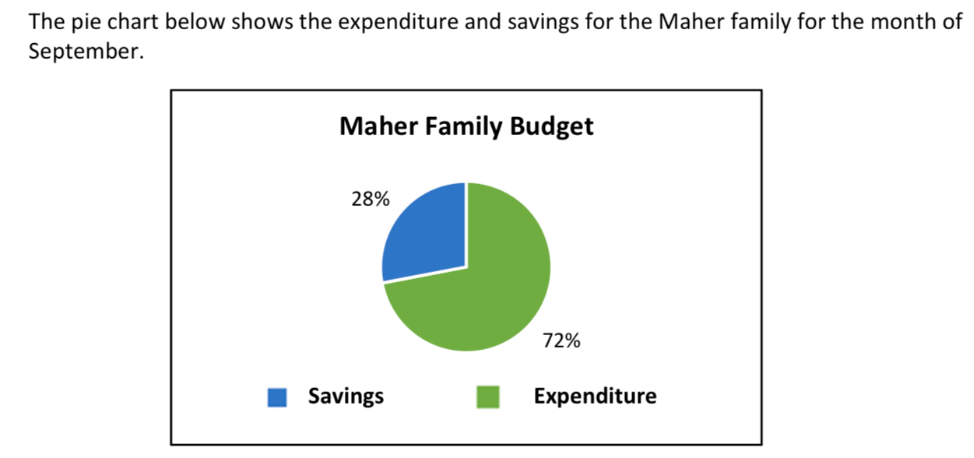

2023 — Q1 — Maher Family Budget Pie Chart

6 marks

(i) The pie chart shows the Maher family spent 72% and saved 28% of their September income of €5,400. Calculate how much money the Maher family saved.

(ii) List three typical sources of household income.

(ii) List three typical sources of household income.

(i) €5,400 × 0.28 = €1,512

(ii) Any three of: Wages / Salary / Overtime • Jobseeker’s Benefit / Social Protection Payments • Child Benefit • Pension • Commission

(ii) Any three of: Wages / Salary / Overtime • Jobseeker’s Benefit / Social Protection Payments • Child Benefit • Pension • Commission

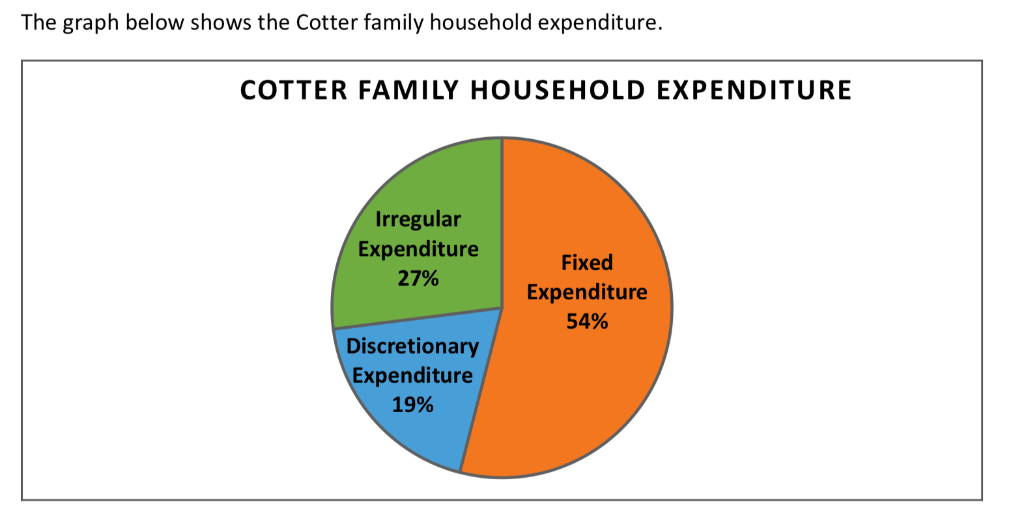

2022 — Q1 — Cotter Family Expenditure Pie Chart

6 marks

(i) Which type of expenditure had the highest percentage?

(ii) Give one example of each type of expenditure.

(ii) Give one example of each type of expenditure.

(i) Fixed Expenditure (54%)

(ii)

Fixed: Mortgage / rent / car loan repayment / TV licence / house insurance

Irregular: Groceries / electricity / car running costs / phone bill / clothing

Discretionary: Entertainment / holidays / gifts / TV subscriptions / restaurant meals

(ii)

Fixed: Mortgage / rent / car loan repayment / TV licence / house insurance

Irregular: Groceries / electricity / car running costs / phone bill / clothing

Discretionary: Entertainment / holidays / gifts / TV subscriptions / restaurant meals

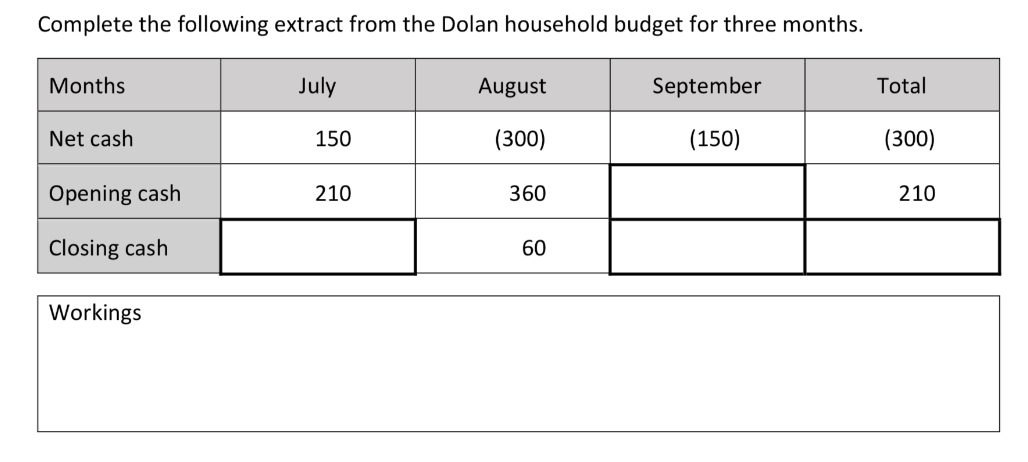

2022 — Q13 — Dolan Household Budget Extract

8 marks

Complete the following extract from the Dolan household budget for three months.

| Months | July € | August € | September € | Total € |

|---|---|---|---|---|

| Net Cash | 150 | (300) | (150) | (300) |

| Opening Cash | 210 | 360 | 60 | 210 |

| Closing Cash | 360 | 60 | (90) | (90) |

Top Tip: Closing cash for one month = opening cash for the next. August closing cash (60) = September opening cash (60). The Total closing cash is always the same as the final month’s closing cash.

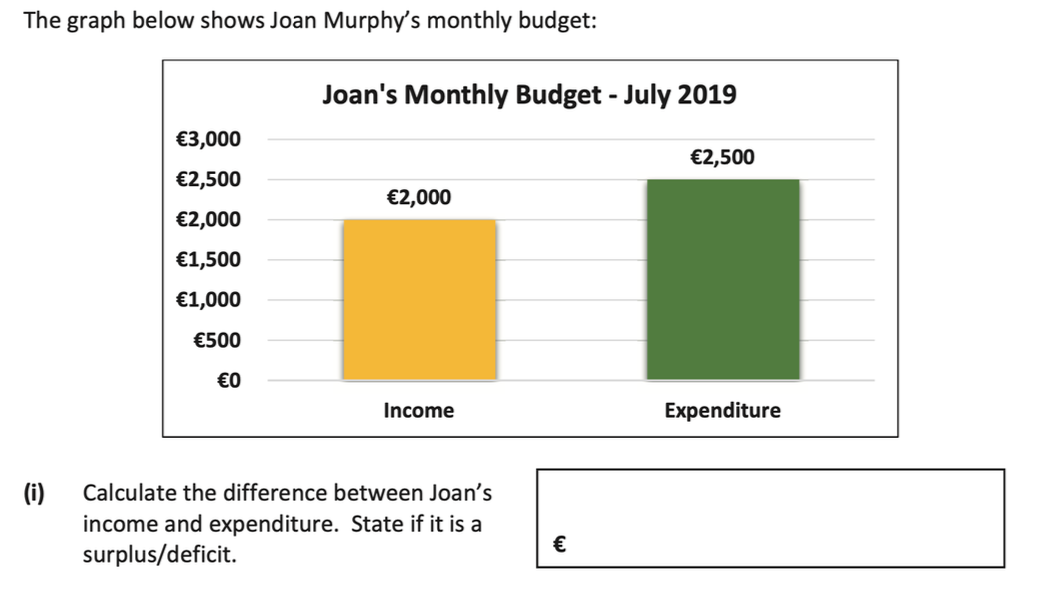

2019 — Q1 — Joan Murphy’s Monthly Budget Graph

6 marks

The graph shows Joan Murphy’s monthly budget for July 2019: Income €2,000 • Expenditure €2,500.

(i) Calculate the difference between Joan’s income and expenditure. State if it is a surplus or deficit.

(ii) What advice would you give Joan based on your answer?

(i) Calculate the difference between Joan’s income and expenditure. State if it is a surplus or deficit.

(ii) What advice would you give Joan based on your answer?

(i) €2,000 − €2,500 = (€500) deficit

(ii) Joan has a deficit of €500. She could:

• Reduce discretionary expenditure — cancel non-essential spending such as entertainment to bring planned expenditure back in line with planned income.

• Increase income — work extra hours or take on a part-time job to increase planned monthly income.

(ii) Joan has a deficit of €500. She could:

• Reduce discretionary expenditure — cancel non-essential spending such as entertainment to bring planned expenditure back in line with planned income.

• Increase income — work extra hours or take on a part-time job to increase planned monthly income.